Workers’ Comp Mistakes Small Businesses Can’t Afford to Make

Ignoring workers’ compensation can be a costly mistake for your small business, leading to unforeseen financial liability and risk exposure. With the right coverage, you protect both your employees and your bottom line. But missteps, like neglecting to purchase coverage or misclassifying employees, can lead to serious financial and legal troubles. Want to steer clear of these pitfalls? Learn about the frequent errors small businesses make and find out how to keep your employees and money safe through practical risk management and safety measures.

What is Workers’ Compensation?

Workers’ compensation is a form of insurance providing wage replacement and medical benefits to employees injured in the course of employment, having covered over 140 million workers in the U.S. as of 2023.

This insurance provides a way for employees to receive medical treatment without needing to take legal action against their employers.

Benefits generally include medical expenses, rehabilitation costs, and disability payments. For example, if an employee fractures a limb on the job, their medical bills would be covered, and they might receive a percentage of their income while they recover.

This system helps injured workers and lowers costs for employers by reducing their legal responsibility.

Importance for Small Businesses

For small businesses, having workers’ compensation can help cover potential legal costs. On average, a claim costs about $40,000, depending on the seriousness of the injury.

Without this coverage, a single workplace injury can devastate a small business financially, increasing risk exposure and highlighting the importance of safety regulations. For instance, a local bakery faced bankruptcy when an employee slipped and fell, leading to over $50,000 in medical expenses and lost wages.

Similarly, a small construction firm lost a critical contract due to legal disputes following an unprotected injury claim, demonstrating the need for proper claim filing and coverage verification.

Tools like BWC insurance calculators can help estimate possible costs, while talking to a local insurance broker can create a policy that meets the business’s needs, providing reassurance and protection against unexpected incidents.

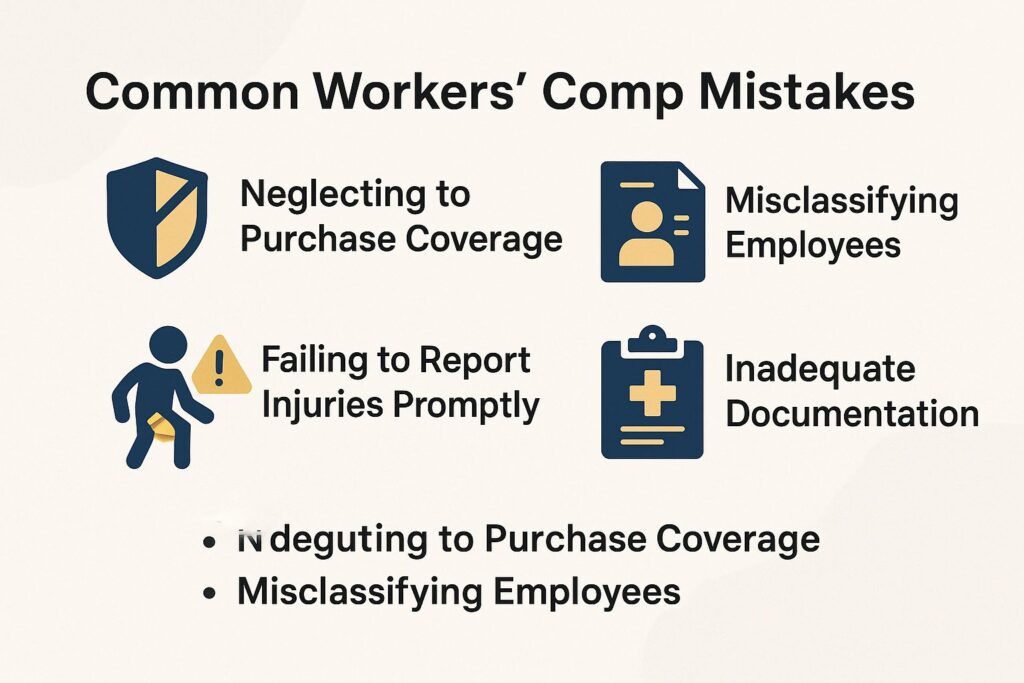

Common Workers’ Comp Mistakes

Small businesses frequently miss important details of workers’ compensation, resulting in expensive errors that can risk their operations and money, including documentation errors and insurance fraud.

Neglecting to Purchase Coverage

Not buying workers’ compensation insurance can result in heavy fines, with the average penalty being $10,000 according to state rules, emphasizing the importance of legal obligations and insurance requirements.

Plus financial penalties, a lack of coverage can expose businesses to legal action from injured employees, highlighting employer liability and the need for legal representation. For instance, a construction firm in New York faced a $250,000 lawsuit after an employee was injured on-site without appropriate insurance.

States might stop companies from operating by taking away their licenses or raising fines, which can interfere with their activities. To prevent these risks, talk to a certified insurance agent to create a workers’ compensation plan that matches your business needs and follows state regulations.

Misclassifying Employees

Misclassifying employees as independent contractors can expose businesses to substantial tax liabilities and fines, with the IRS estimating an annual loss of $3 billion due to misclassification.

To correctly classify employees, businesses should evaluate specific criteria, such as the degree of control over work and the nature of the working relationship.

For instance, the IRS uses the “20-Factor Test,” which considers aspects like supervision and provision of tools.

In recent years, companies like Uber and Lyft faced multi-million dollar penalties for misclassifying drivers, highlighting the importance of clear distinctions.

Using correct categorization helps secure financial security and creates an open work environment.

Failing to Report Injuries Promptly

Reporting injuries quickly is important because delays can lead to rejected claims and legal issues that might be expensive for businesses.

Injuries should typically be reported within 24 to 72 hours, depending on state regulations, reinforcing the importance of claims timelines and accident reporting. Missing these deadlines can harm the claim and damage the trust between employers and employees.

To avoid complications, follow this checklist:

- Document the injury and circumstances immediately.

- Notify supervisors or HR without delay.

- Seek medical attention promptly.

- Complete the necessary incident report and any required forms.

- Contact your insurance company to make sure they handle your claim quickly.

Staying proactive can make a significant difference in claim outcomes.

Inadequate Documentation

Inadequate documentation of workplace injuries can result in claim disputes, with 30% of claims being denied due to lack of proper records.

To support claims, keep thorough records with detailed incident reports, statements from witnesses, and medical assessments, following best practices in claims process and policyholder obligations.

Use a centralized document management system, like Google Drive or Dropbox, to organize these records by date or type of incident.

For example, a well-documented claim could contain a signed incident report that outlines the circumstances, along with a physician’s note indicating the nature of the injury.

This organized method supports the claim and helps create a safer workplace by finding trends in incidents.

Understanding Employee Classification

Understanding how employees are categorized is crucial for adhering to regulations and managing finances, particularly when navigating complex federal regulations and employment law. It impacts insurance and payment claims significantly. To ensure your business remains compliant with labor laws, you might benefit from exploring our Labor Law Compliance Checklist which provides a straightforward approach to identifying potential risks.

Independent Contractors vs. Employees

The distinction between independent contractors and employees directly impacts workers’ compensation obligations, with only 30% of contractors being eligible for benefits.

This classification depends on various factors, such as how work is directed, financial oversight, and the connection between the parties.

For instance, an employee typically operates under direct supervision, receiving training and benefits from the employer, such as health insurance. In contrast, an independent contractor like a freelance graphic designer manages their own clients and schedules, often providing tools and services based on contracts.

Knowing these differences is important for businesses to follow labor laws and prevent possible fines.

Implications of Misclassification

Misclassification can lead to significant legal repercussions, including back pay for benefits and fines that may exceed $50,000 in some cases.

Businesses face potential lawsuits from misclassified employees, leading to costly settlements. According to the IRS, misclassification can result in unpaid payroll taxes that may double the amount owed.

For instance, a misclassified employee earning $50,000 could lead to $15,000 in back taxes and penalties. Operationally, it can damage workplace morale, as properly classified employees may feel undervalued or mistreated.

To prevent these problems, frequently check your classification methods and talk to legal or HR experts to follow labor laws correctly.

Reporting and Filing Claims

Knowing how to report and file claims is important to make sure employees get their benefits on time, ensuring claims experience and compliance audits.

Steps to Report an Injury

To report an injury, employers should take these steps, focusing on safety training and employee communication:

- Inform the employee,

- Record the details of the incident,

- Fill out the required paperwork,

- Submit claims to the insurance company within 30 days.

After notifying the employee, gather details about the injury. This includes the time, location, and circumstances surrounding the incident. Use forms like the OSHA 301 to document the specifics.

Next, collect witness statements if applicable, which can support the claim. Once all documentation is completed, submit it immediately, ensuring compliance with state laws and insurance requirements about timely submissions.

By following these steps, you meet legal requirements and make the workplace safer by explaining what happened in an incident.

Common Filing Errors

Filing errors can lead to claim denials; common pitfalls include incorrect dates, missing signatures, and incomplete documentation-which account for approximately 20% of all claims.

One prevalent mistake is failing to provide all required supporting documents. For example, a homeowner’s claim for storm damage may be denied if repair estimates are absent. Submitting the claim without a signature can result in immediate rejection.

To avoid these issues, double-check submission requirements for your specific insurance policy, keep an organized filing system for all relevant documents, and confirm all necessary signatures before submitting.

Using a checklist can greatly simplify this process, helping you avoid missing important parts.

Staying Compliant with Regulations

It’s important to follow workers’ compensation rules to avoid risks and fines because laws vary significantly between states, influencing policy renewals and legal compliance.

State-Specific Requirements

Each state has distinct workers’ compensation requirements; for example, Texas allows businesses not to carry coverage, while California mandates it for all employers, impacting claim settlement and insurance discounts.

States like New York and Florida require coverage for businesses with a small number of employees, often as few as one or two.

Non-compliance penalties vary significantly; for instance, failing to provide coverage in California can result in fines of up to $10,000, while New York may impose a fine of $2,000 per 10-day period.

Employers need to check their state’s rules and talk to a lawyer or use a compliance tool to prevent expensive errors.

Regular Policy Review and Updates

Regularly checking and updating your workers’ compensation policy can help keep it compliant and provide enough coverage for your business, considering coverage options and policy limits. An annual review is a good practice.

During the review, focus on key elements such as coverage limits, employee classifications, insurance coverage, and state-specific regulations.

For instance, if you’ve hired new employees with different roles, adjust classifications to avoid underpayment or overpayment of premiums. Monitor changes in laws or regulations that could affect your obligations.

Using tools like a compliance checklist or consulting with a workers’ compensation expert can simplify this process. Keeping detailed records of changes allows you to revisit choices if necessary.

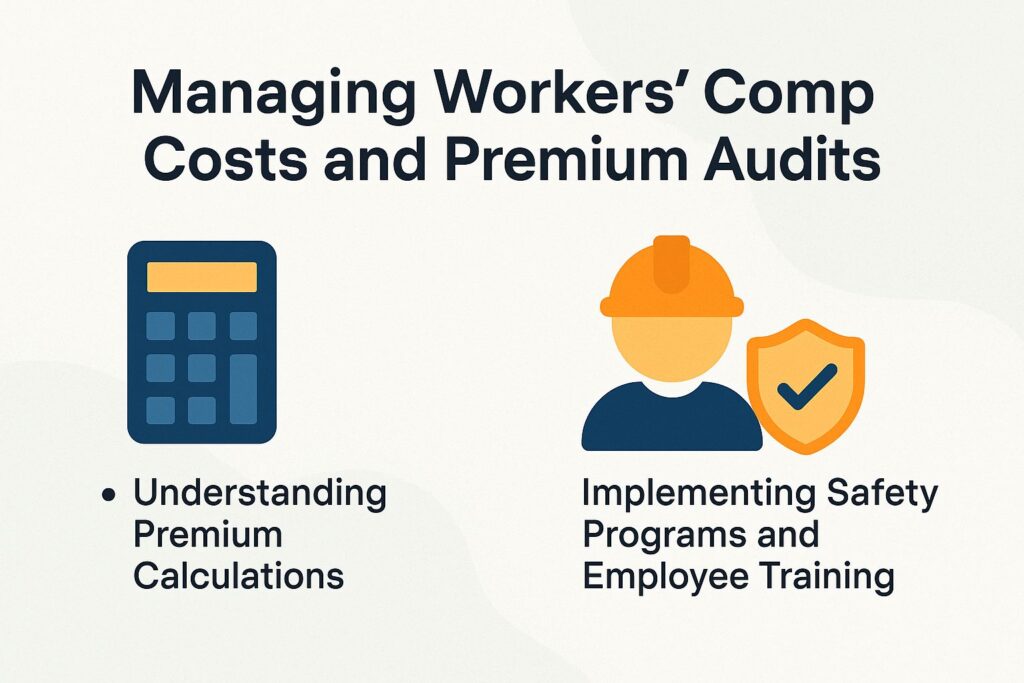

Managing Workers’ Comp Costs and Premium Audits

Keeping workers’ compensation expenses in check is important for small businesses. These expenses usually fall between $0.75 and $2.74 for each $100 of payroll. One of our most insightful case studies explains how a Professional Employer Organization (PEO) can assist in managing and reducing these costs effectively.

Understanding Premium Calculations

Knowing how insurance rates are figured out can help businesses predict expenses. Rates depend on the size of the payroll, the risk level of the industry, and the history of claims.

To break down these factors, use the following formula:

Premium = (Payroll x Rate per $100) x (Experience Modifier).

For instance, if your business has a payroll of $200,000 in a classification with a rate of $1.50, the base premium would be $3,000. If your experience modifier is 0.90 (indicating fewer claims), your final premium would be $2,700.

Monitoring claims and maintaining safety protocols, along with effective injury prevention strategies, can significantly influence these calculations, proving beneficial for long-term cost management.

Implementing Safety Programs and Employee Training

Implementing thorough safety programs can reduce workplace injuries by up to 50%, which decreases workers’ compensation expenses and improves employee morale.

For effective safety programs, small businesses should focus on employee training, carry out regular safety checks, and involve employees in safety talks.

Monthly safety meetings give employees a chance to talk about issues and offer ideas for better practices. Meanwhile, tools like SafetyCulture can make audits more organized and keep an eye on rules being followed.

Offering practical training with examples specific to your company’s environment promotes a safety-focused mindset. Companies like Varied Industries have successfully reduced incidents by including team members in developing programs, demonstrating that participation increases both awareness and commitment to safety.

Dealing with Claims, Disputes, and Insurance Policy Reviews

Handling claims and disagreements in workers’ compensation means knowing typical problems such as denial of claims and finding good ways to solve them.

Common Reasons for Claim Denials and Insurer Negligence

Common reasons for workers’ comp claim denials include failure to report injuries on time, lack of medical documentation, and employer negligence, accounting for nearly 25% of claims.

- To improve your chances of a successful claim, report any injury to your supervisor within 24 hours.

- Get complete medical papers, like diagnosis and treatment records, from your doctor.

- Check that your employer has filed the necessary paperwork on their end. Regularly following up on the status of your claim can also mitigate issues, as it demonstrates your commitment and keeps you informed about any outstanding requirements.

How to Appeal a Denied Claim

- Read the denial letter carefully.

- Collect documents that support your case.

- Submit an appeal by the deadline.

- Consult a lawyer if needed.

Begin by clearly identifying why you were denied, such as policy exclusions, as this will help you plan your appeal.

Gather important papers, like medical records, work accident reports, witness statements, and claim follow-ups to strengthen your case.

Make sure to submit your appeal within the state-mandated period, often limited to 30 days, considering litigation risks.

If your appeal is unsuccessful, consider examples like one claimant who successfully overturned a denial by providing additional medical evidence and testimony from a treating physician.

Getting legal advice can improve the likelihood of a positive result.

Creating a Culture of Safety and Organizational Culture

Establishing a culture of safety involves regular training, open communication about hazards, and employee involvement in safety protocols, which can decrease accidents by over 40%.

One effective strategy is implementing bi-annual safety training programs, such as OSHA-compliant workshops, which familiarize employees with standards, regulatory compliance, and practices.

Promote regular safety meetings where workers can discuss possible dangers and suggest ways to fix them.

Create a safety group made up of frontline workers and a safety committee to make sure ideas are listened to and implemented.

Tools like SafetyCulture help monitor safety checks and quickly solve problems, encouraging active attention to workplace safety and employee wellness.

Written by Carol Sanders

Harvard University graduate with a degree in psychology and human resources.

Owner of a PEO consulting firm in Massachusetts and contributing writer for PEO Costs.